Your 2026 Homeownership Roadmap: Smart Strategies for Buying, Refinancing, and Building Wealth

Expert insights from The Mortgage Squad, serving Wichita, Topeka, and all of Kansas.

As we look toward 2026, the landscape of homeownership in Kansas is evolving. Whether you are looking to purchase your first home in Wichita, build a custom property in Andover, or leverage the equity you’ve built in Topeka, having a strategic roadmap is essential. The real estate market is no longer just about interest rates; it is about matching your long-term financial goals with the right mortgage products.

At The Mortgage Squad, powered by LeaderOne Financial, we believe that a mortgage isn’t just a loan—it’s a financial tool. Randy Pitts and David Chittwood have spent years guiding Kansans through market shifts, helping families build wealth through smart real estate decisions. This guide is your comprehensive roadmap to navigating the 2026 housing market with confidence.

The 2026 Kansas Market Outlook: What to Expect

The Wichita and Topeka housing markets have shown incredible resilience. With median home prices in Wichita hovering around a competitive range compared to the national average, our local market remains an attractive hub for families and investors alike. As we approach 2026, we anticipate a continued “heating up” of the market, particularly in suburban areas like Andover and Sedgwick County.

However, inventory fluctuations mean buyers need to be prepared. The days of waiting on the sidelines are over; strategic action is the theme for the coming year. Whether rates stabilize or fluctuate, the key to success lies in preparation and utilizing the diverse loan programs available to

you.

Smart Buying Strategies for Every Borrower

One size does not fit all when it comes to mortgages. To secure your dream home in 2026, you need to align your borrower profile with the specific loan type that offers you the most leverage.

1. First-Time Homebuyers: Breaking the Rent Cycle

If you are currently renting, 2026 is the year to lock in your housing costs. Rents in Wichita and Topeka are subject to inflation, but a fixed-rate mortgage ensures stability. We offer several programs specifically designed to lower the barrier to entry:

- FHA Loans: Perfect for buyers with lower credit scores or smaller down payments (as low as 3.5%). This is a forgiving program that helps many families get the keys to their first home.

- USDA Loans: If you are looking to buy in qualifying rural areas outside of the major city centers, you might qualify for 100% financing. This means $0 down payment.

- Down Payment Assistance (DPA): We actively help clients access DPA programs. These can provide grants or second liens to cover your down payment and closing costs, keeping cash in your pocket.

Tip: Don’t assume you need 20% down. Explore our First-Time Homebuyer Programs to see how little you actually need to get started.

2. Veterans and Active Military: Maximizing Your Benefits

We are honored to serve those who have served. VA Loans remain one of the most powerful wealth-building tools available. With $0 down payment requirements and no monthly mortgage insurance (PMI), VA loans often offer lower interest rates than conventional financing.

Randy Pitts and the team understand the nuances of VA guidelines, ensuring you get the most out of your entitlement. Whether you are stationed in Kansas or retiring here, this loan is the gold standard for veteran homeownership.

3. Self-Employed and Gig Economy Workers: Non-QM Loans

The workforce has changed, and traditional banks haven’t always kept up. If you are a business owner, freelancer, or gig worker in Wichita, you might show a lower net income on tax returns due to write-offs. That shouldn’t disqualify you from a mortgage.

Non-QM (Non-Qualified Mortgage) Loans allow us to qualify you based on alternative methods, such as bank statements or asset depletion, rather than just W-2 forms. This is a game-changer for entrepreneurs looking to buy in 2026.

Building Wealth: Construction and Investment

For many, the roadmap to 2026 involves more than just buying an existing house; it involves creating value.

Constructing Your Dream Home

Inventory shortages can be frustrating. Sometimes, the best strategy is to build exactly what you want. Our Construction Loans offer short-term financing to cover the cost of building the home, which is then converted into a permanent mortgage upon completion.

Whether you are building on a lot in a new development in Topeka or a custom build in Andover, we manage the draw process to keep your builder paid and your project on track.

Real Estate Investing

Building wealth often means diversifying your portfolio. Wichita’s strong rental market makes it an excellent location for investment properties. We offer specialized Loan Programs for Investors, including options for rental properties and fix-and-flips. By leveraging leverage (using a mortgage to buy an asset), you can increase your cash-on-cash return compared to paying cash outright.

Refinancing: Strategic Moves for Homeowners

If you already own a home, your roadmap for 2026 should include a mortgage review. Refinancing isn’t just about lowering your rate; it’s about restructuring your debt to meet your goals.

Rate-and-Term Refinance

If interest rates dip in 2026, a rate-and-term refinance can lower your monthly payment, improving your monthly cash flow. Even a small reduction in rate can save thousands over the life of the loan.

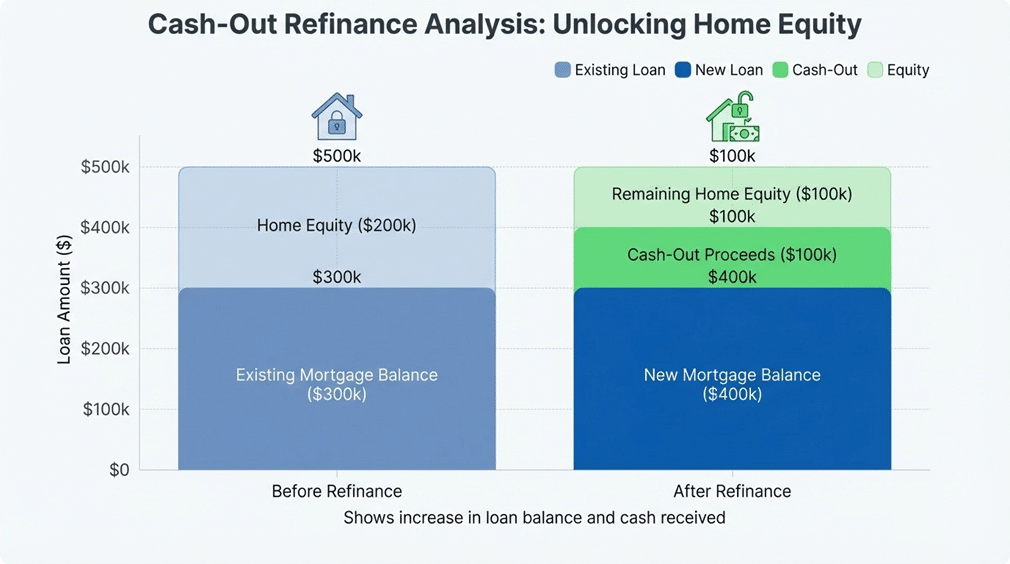

Cash-Out Refinance

Home values in Kansas have appreciated. You likely have significant equity sitting in your home. A Cash-Out Refinance allows you to tap into that wealth to:

- Pay off high-interest credit card debt (consolidating debt often lowers total monthly payments significantly).

- Fund home renovations (kitchens, baths, or additions).

- Pay for college tuition or other major life expenses.

We can help you run a “break-even analysis” to see if refinancing makes financial sense for your specific situation.

Specialized Solutions: Reverse Mortgages

For our clients aged 62 and older, the goal often shifts from “building” wealth to “accessing” wealth to enjoy retirement. A Reverse Mortgage allows you to convert part of the equity in your home into cash without having to sell the home or make additional monthly mortgage payments.

This can provide funds for healthcare, daily living expenses, or simply improving your quality of life. It is a sophisticated financial tool, and Randy and David are here to help you understand if it fits your retirement roadmap.

Loan Program Comparison Guide

| Loan Program | Best For | Key Benefit |

| Conventional | Borrowers with good credit (620+) | Flexible terms, adjustable PMI |

| FHA Loan | First-time buyers, lower credit scores | Low down payment (3.5%), lenient |

| VA Loan | Veterans and Active Military | 0% Down, No Mortgage Insurance. |

| USDA Loan | Rural homebuyers | 0% Down payment for eligible rural |

| Non-QM | Self-employed / Gig workers | Qualify using bank statements, not |

| Reverse Mortgage | Homeowners 62+ | Access equity with no monthly |

Frequently Asked Questions (FAQs)

1. What credit score do I need to buy a house in Wichita in 2026?

2. How much down payment is really required?

Many buyers believe they need 20% down, but that is a myth. FHA loans require 3.5%, Conventional loans can go as low as 3% for first-time buyers, and VA and USDA loans offer 0% down payment options for qualified borrowers. We also work with Down Payment Assistance programs that can help cover these costs.

3. Is 2026 a good time to refinance my home?

It depends on your current interest rate and your financial goals. If market rates drop below your current rate, refinancing can lower your payment. Alternatively, if you have high-interest debt (like credit cards), a cash-out refinance might save you money monthly even if the mortgage rate is slightly higher, by consolidating that debt into one tax-deductible payment.

4. What is the difference between a Mortgage Banker and a Bank?

As Mortgage Bankers/Brokers, The Mortgage Squad has access to a wide variety of loan products from multiple investors, rather than just the limited products of a single bank. This allows us to “shop” for the best rates and terms specifically for your situation, whether you are in Wichita, Topeka, or anywhere in Kansas.

5. How does a construction loan work if I want to build?

A construction loan is a short-term loan used to pay for the cost of building your home. Funds are paid out in “draws” to the builder as work is completed. Once the home is finished, the loan is converted into a permanent mortgage (like a 30-year fixed). We guide you through both the construction phase and the permanent financing phase.

Start Your Journey with The Mortgage Squad

Your roadmap to homeownership in 2026 starts with a conversation. Whether you are ready to apply today or just starting to plan for next year, getting pre-approved gives you the competitive edge you need in the Kansas market.

Randy Pitts (Wichita) and David Chittwood (Topeka) are ready to help you navigate your options. Don’t leave your financial future to chance—partner with a team that treats your mortgage like the investment it is.