Your 2026 Homeownership Roadmap: Smart Strategies for Buying, Refinancing, and Building Wealth

As we move into 2026, the real estate landscape in Topeka, Kansas continues to evolve. Whether you are looking to plant roots in Topeka, expand your investment portfolio in Wichita, or leverage the equity in your current home, having a strategic plan is essential. The days of guessing your way through a mortgage are over; today’s market requires a roadmap tailored to your financial goals.

At The Mortgage Squad, powered by LeaderOne Financial, we don’t just write loans; we build strategies. With David Chittwood leading the charge in Topeka and Randy Pitts serving Wichita, our team is dedicated to guiding you through the complexities of the 2026 housing market. This comprehensive guide outlines smart strategies for buying, refinancing, and building long-term wealth through real estate.

Phase 1: The Buying Strategy – Navigating the 2026 Market

Buying a home remains one of the most reliable ways to build generational wealth. However, the “one-size-fits-all” mortgage approach is obsolete. To succeed in 2026, you need to match your financial profile with the specific loan product that maximizes your purchasing power.

1. First-Time Homebuyers: Breaking Down Barriers

If 2026 is the year you transition from renting to owning, understanding your entry points is critical. Many buyers in Topeka assume they need a 20% down payment, but that is a myth that keeps too many renters on the sidelines.

- FHA Loans: Perfect for buyers with lower credit scores or limited savings. With down payments as low as 3.5%, an FHA loan allows you to enter the market sooner rather than later.

- Down Payment Assistance: We actively help clients in Kansas identify local and state programs that can cover upfront costs. Don’t let the initial cash requirement stop you from building equity.

2. Rural Development: The USDA Advantage

Kansas offers unique opportunities for those willing to live slightly outside major city centers. USDA Loans provide 100% financing—meaning zero down payment—for eligible properties in designated rural areas. This is often an overlooked strategy for buyers in the outskirts of Topeka and Wichita who want more land and less upfront cost.

3. Honoring Service: VA Loans

For our active-duty military and veterans, the VA Loan remains the gold standard of home financing. It offers $0 down payment, no private mortgage insurance (PMI), and typically lower interest rates. David Chittwood and The Mortgage Squad team specialize in helping veterans navigate the Certificate of Eligibility (COE) process to maximize this earned benefit.

4. Building vs. Buying: Construction Loans

Inventory shortages can sometimes make finding the “perfect” home difficult. In 2026, more buyers are choosing to build. Our Construction Loans are designed to simplify this process. Unlike traditional mortgages, these loans release funds in phases (draws) as construction milestones are met. Once the home is complete, we can seamlessly transition you into a permanent mortgage. This “one-time close” option saves you money on closing costs and reduces stress.

Phase 2: The Wealth Building Strategy – Investing and Non-Traditional Income

Real estate is not just about having a place to sleep; it’s an investment vehicle. As we navigate 2026, savvy borrowers are looking beyond their primary residence.

Investment Property Loans

Whether you are looking to buy a duplex in Topeka or a rental property in Wichita, Investor Loans are key to scaling your portfolio. We offer specialized financing solutions for rental and resale properties, including multi-unit property loans. By leveraging rental income to qualify, you can expand your assets without overextending your personal debt-to-income ratio.

Non-QM Loans: Solutions for the Self-Employed

The “gig economy” and entrepreneurship are booming in Kansas. However, traditional banks often struggle to underwrite loans for business owners who write off expenses to lower their taxable income. This is where Non-QM (Non-Qualified Mortgage) Loans shine.

We can qualify borrowers based on:

- Bank Statements: Using 12-24 months of business bank statements to calculate income rather than tax returns.

- Asset Depletion: Using your liquid assets to calculate a monthly income stream.

- DSCR (Debt Service Coverage Ratio): For investors, qualifying based on the cash flow of the property itself, rather than personal income.

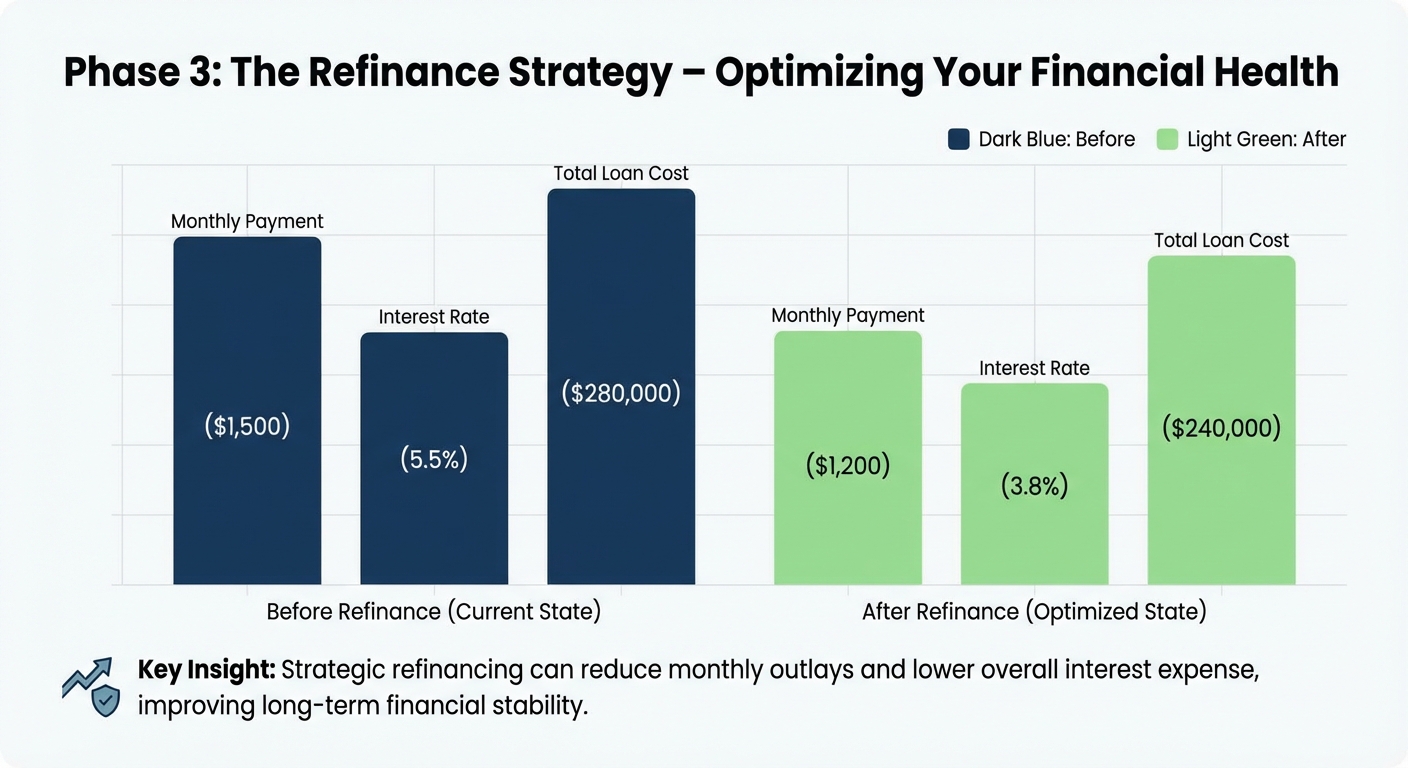

Phase 3: The Refinance Strategy – optimizing Your Financial Health

Cash-Out Refinance for Debt Consolidation

With consumer credit card debt at all-time highs, high-interest payments can suffocate your monthly budget. A Debt Consolidation Refinance allows you to tap into your home’s equity to pay off high-interest credit cards, personal loans, or medical bills. By rolling these into a tax-deductible mortgage payment (consult your tax advisor), you can often lower your total monthly outflow by hundreds of dollars, significantly improving your cash flow.

Rate and Term Refinance

Reverse Mortgages: Financial Freedom for Seniors

For homeowners aged 62 and older, a Reverse Mortgage can be a strategic part of a retirement roadmap. This allows you to convert part of your home equity into cash without having to sell your home or make monthly mortgage payments. It is an excellent tool for supplementing retirement income, covering medical expenses, or funding home modifications to age in place comfortably.

Comparing Your Loan Options

| Loan Type | Ideal For | Down Payment | Key Benefit |

|---|---|---|---|

| Conventional | Borrowers with good credit (620+) | 3% – 20% | Flexible terms, no PMI with 20% equity. |

| FHA Loan | First-time buyers & credit challenged | 3.5% | Easier credit qualification & low down payment. |

| VA Loan | Veterans & Active Military | 0% | No PMI, competitive rates, 100% financing. |

| USDA Loan | Rural homebuyers | 0% | 100% financing for eligible rural areas. |

| Construction Loan | Building a custom home | Varies | Interest-only payments during construction. |

| Non-QM | Self-employed & Investors | Varies | Alternative income verification (Bank statements). |

Why Local Expertise Matters in Topeka and Wichita

Real estate is hyper-local. A national call center lender doesn’t understand the nuances of the Topeka housing market or the rural eligibility maps surrounding Wichita. When you work with David Chittwood and The Mortgage Squad, you are getting:

- Accessibility: We are based here. You can call David at 1-785-450-9056 or email DavidChittwood@leader1.com and get a real person, not a chatbot.

- Speed: In a competitive market, closing speed matters. We handle our processing efficiently to get you to the closing table on time.

- Customization: We review your entire financial picture to suggest the roadmap that builds wealth, not just the loan that gets you a house.

Frequently Asked Questions (FAQs)

1. Is 2026 a good year to buy a home in Topeka, KS?

While market conditions fluctuate, owning a home remains a strong hedge against inflation. Topeka continues to offer affordable housing compared to the national average. By utilizing programs like FHA or USDA loans, you can lock in your housing costs, unlike renting where costs typically rise annually.

2. How does a Construction Loan differ from a regular mortgage?

A standard mortgage pays for a completed home in full. A construction loan pays the builder in “draws” or stages as the house is built. During construction, you typically only pay interest on the funds that have been paid out. Once the home is finished, the loan converts to a permanent mortgage.

3. Can I use a Cash-Out Refinance to pay off credit card debt?

Yes, this is one of the most common uses for a cash-out refinance. Mortgage interest rates are typically much lower than credit card interest rates. By consolidating debt, you can lower your total monthly payments and make the interest tax-deductible (consult a tax professional).

4. What if I am self-employed and don’t show enough income on my tax returns?

This is a common scenario for business owners. We offer Non-QM (Non-Qualified Mortgage) loans that allow us to verify your income using personal or business bank statements over 12 to 24 months, rather than looking at the net income on your tax returns.

5. Do I need a 20% down payment to avoid PMI?

Not necessarily. While 20% down eliminates Private Mortgage Insurance (PMI) on conventional loans immediately, you can buy with as little as 3% or 3.5% down. On conventional loans, PMI can eventually be removed once you build enough equity. On VA loans, there is no PMI regardless of the down payment.

Ready to Start Your Journey?

Your 2026 homeownership roadmap starts with a conversation. Don’t navigate the market alone. Whether you are looking to buy your first home in Topeka, build your dream house, or refinance to consolidate debt, The Mortgage Squad is here to serve you.

Contact David Chittwood today to get pre-qualified or discuss your refinancing options.

Phone: 1-785-450-9056

Email: DavidChittwood@leader1.com

Click Here to Apply Now

The Mortgage Squad is powered by LeaderOne Financial Corporation. NMLS #12007. David Chittwood NMLS #1868247. 149 S Andover Rd, Andover, KS 67002. This is not an offer to lend. All loans are subject to credit approval. Programs, rates, terms, and conditions are subject to change without notice. Equal Housing Lender.