Preparing for the Spring Market Rush: A Homebuyer’s Guide for Wichita & Topeka

By Randy Pitts | The Mortgage Squad, Powered by LeaderOne Financial

As the winter chill begins to fade across Kansas, the real estate market is doing exactly what the flowers are preparing to do: bloom. In the mortgage and real estate industry, we call this the Spring Market Rush. It is traditionally the busiest, most competitive, and most exciting time of the year to buy a home in Wichita and the surrounding areas like Andover.

Whether you are a first-time homebuyer looking for a starter home in Riverside or an experienced investor scouting properties in Topeka, entering the spring market without a strategy is a risky move. Inventory moves faster, bidding wars become more common, and the window of opportunity to lock in a great rate can narrow quickly.

At The Mortgage Squad, led by Randy Pitts (Wichita), we believe that preparation is the key to success. This comprehensive guide will walk you through exactly how to prepare your finances, your mindset, and your team for the upcoming spring frenzy.

Why the Spring Market is Different in Kansas

Real estate is seasonal. While people buy and sell homes year-round, spring (typically defined as March through June) sees a significant spike in activity. Families often want to move before the next school year starts, and curb appeal is at its peak when the grass turns green.

For buyers in Wichita, KS, this means two things:

- More Inventory: You will see more “For Sale” signs popping up in yards than you did in December or January.

- More Competition: You aren’t the only one who waited for the snow to melt. More buyers mean you need to be faster and stronger with your offers.

To navigate this dynamic environment, you need a plan. Here is your step-by-step roadmap to winning in the spring market.

Step 1: The Pre-Approval Advantage

In a relaxed market, you might get away with casual window shopping. In the spring market rush, a mortgage pre-approval is your ticket to entry. Many sellers in competitive areas won’t even entertain an offer unless it is accompanied by a solid pre-approval letter from a reputable local lender.

Pre-Qualification vs. Pre-Approval

It is vital to understand the difference. A pre-qualification is a rough estimate of what you might be able to borrow based on self-reported data. It’s good for a general idea, but it holds little weight at the negotiating table.

A pre-approval, which we specialize in at The Mortgage Squad, involves a verified review of your financial documents (income, assets, credit). When you have a pre-approval from Randy Pitts or David Chittwood, it tells the seller: “This buyer is serious, their finances are vetted, and they can close this deal.”

Action Item: Don’t wait until you find the perfect house. Contact us today to start your pre-approval process so you are ready to strike when the right listing hits the market.

Step 2: Know Your Numbers (Beyond the Interest Rate)

Interest rates are important, but they are only one piece of the puzzle. Preparing for the spring market means understanding your total “comfort zone” for a monthly payment.

When calculating your budget, ensure you are factoring in:

- Principal & Interest: The core of your loan payment.

- Property Taxes: These vary significantly between Sedgwick County and Shawnee County.

- Homeowners Insurance: Essential for protecting your investment against Kansas weather.

- PMI (Private Mortgage Insurance): If you are putting down less than 20% on a conventional loan.

We recommend using our Mortgage Calculator to run different scenarios. However, nothing beats a one-on-one consultation. We can look at your debt-to-income ratio and help you determine a maximum purchase price that keeps you financially comfortable, not just “qualified.”

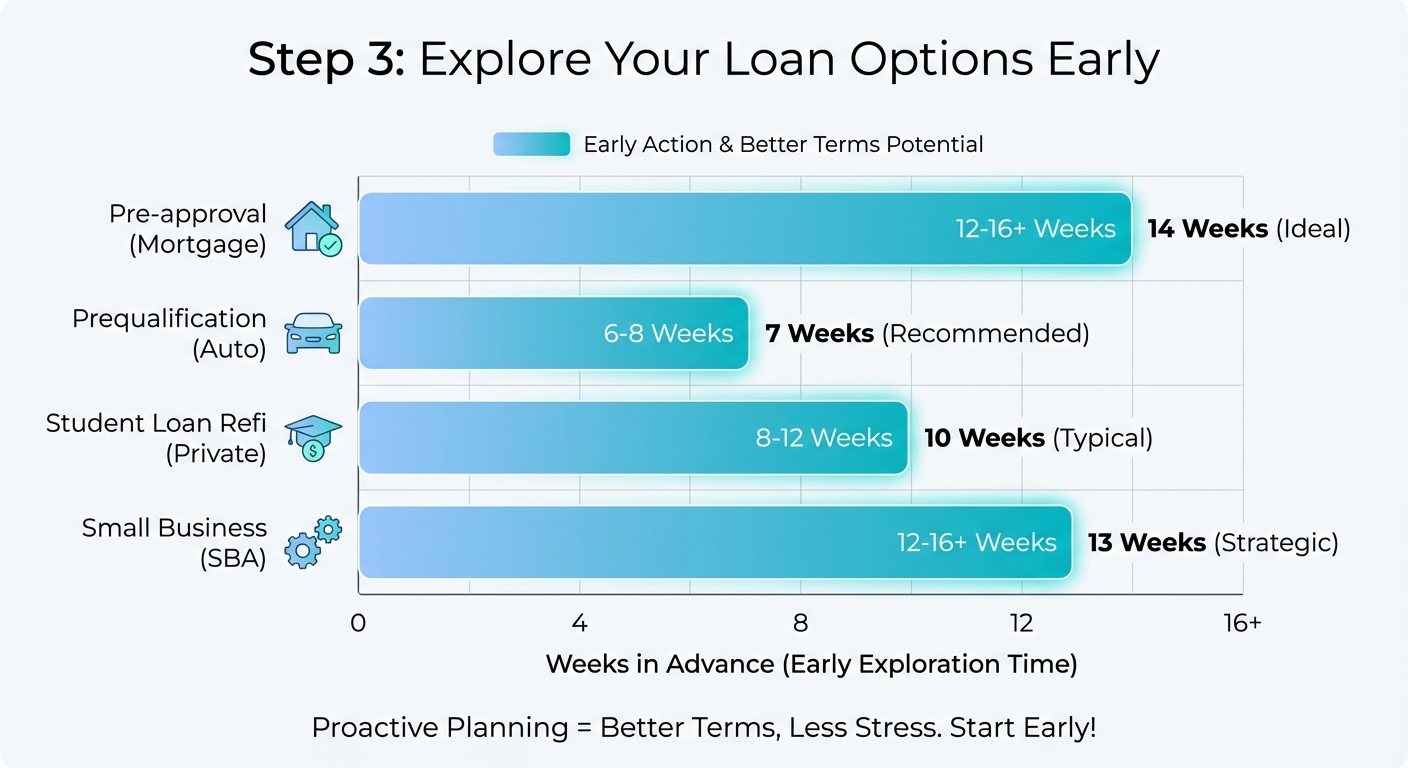

Step 3: explore Your Loan Options Early

Common Loan Types in Kansas:

- Conventional Loans: Great for buyers with good credit and stable income. Offers competitive rates and flexible down payment options.

- FHA Loans: An excellent choice for first-time buyers or those with lower credit scores. The down payment requirement is as low as 3.5%.

- VA Loans: For our veterans and active-duty service members in Wichita and beyond, this is arguably the best loan product available. It often requires $0 down and has no PMI.

- USDA Loans: Looking for a home in a rural area just outside of Wichita? You might qualify for 100% financing through the USDA program.

- Non-QM Loans: If you are self-employed or have non-traditional income, we have specialized solutions for you.

Step 4: Assemble Your Local Squad

Why Local Matters:

- Reputation: Listing agents in Wichita know Randy Pitts and The Mortgage Squad. When they see our name on your pre-approval letter, they know the loan will close on time. This can be the tie-breaker in a multiple-offer situation.

- Communication: The spring market moves fast. You need a team that answers the phone on weekends and evenings when offers are being written.

- Local Knowledge: We know the difference in tax rates between Andover and Wichita, and we know which local grants or down payment assistance programs you might be eligible for.

Strategic Tips for Winning a Bidding War

In the height of the spring market, you may find yourself competing with other buyers for the same property. Here are three expert strategies to make your offer stand out:

- The Speed of the Pre-Approval: As mentioned, have this ready before you tour homes.

- Keep Contingencies Clean: Work with your realtor to see if there are contingencies you can shorten or waive (without putting yourself at undue risk).

- Offer a Strong Earnest Money Deposit: Putting a little more money down as a “good faith” deposit shows the seller you are serious and committed.

Winter vs. Spring Buying: What to Expect

| Feature | Winter Market (Off-Peak) | Spring Market (The Rush) |

|---|---|---|

| Inventory Levels | Lower. Fewer homes to choose from. | High. Many new listings weekly. |

| Competition | Low. You may be the only offer. | High. Multiple offers are common. |

| Negotiation Power | Higher. Sellers may be motivated to move. | Lower. Sellers hold more leverage. |

| Speed of Sale | Slower. Homes sit on the market longer. | Fast. Ideally priced homes sell in days. |

| Price Trends | Often stable or slightly lower. | Often higher due to demand. |

Ready to Join the Squad?

The spring market offers incredible opportunities for homebuyers in Kansas, but it rewards those who are prepared. Don’t let the rush overwhelm you. By partnering with The Mortgage Squad, you are gaining a team of experts dedicated to making your homeownership dreams a reality.

Whether you are in Wichita, or anywhere in between, Randy Pitts are here to guide you through every step of the mortgage process.

Get Started Today!

Don’t wait for the perfect home to hit the market before you talk to a lender. Get pre-approved now so you can shop with confidence.

Call Randy Pitts: 316-559-2600

Email: RandyPitts@leader1.com

Visit Us: TheMortgage-Squad.com

Frequently Asked Questions (FAQs)

1. When should I start the mortgage process for a spring home purchase?

Ideally, you should start the pre-approval process 60 to 90 days before you plan to buy. This gives you time to correct any errors on your credit report, save for a down payment, and clarify your budget before the market heats up.

2. Does getting pre-approved hurt my credit score?

A pre-approval requires a “hard inquiry” on your credit, which may lower your score by a few points temporarily (usually less than 5 points). However, the benefit of knowing your buying power and being able to submit a valid offer far outweighs this minor, temporary dip.

3. What documents do I need to provide to The Mortgage Squad?

To get a verified pre-approval, be prepared to provide: W-2s for the last two years, recent pay stubs (last 30 days), bank statements (last 2 months), and tax returns if you are self-employed. Having these ready speeds up the process significantly.

4. Can I still buy a home in the spring if I have a low credit score?

Yes! We work with many clients who have less-than-perfect credit. FHA loans, for example, have more lenient credit requirements than conventional loans. We can also provide advice on how to improve your score quickly to qualify for better terms.

5. Is it better to use a local lender in Wichita or a big national bank?

Using a local lender like The Mortgage Squad offers distinct advantages in a competitive market. We understand the local real estate landscape, we have relationships with local appraisers and agents, and we are accessible when you need us. National call centers often cannot move fast enough for the Wichita spring market.