Master Your Finances: Using a Mortgage Refinance for Debt Management in Wichita, KS

Are high-interest credit card bills, personal loans, or medical debt keeping you up at night? You are not alone. Many homeowners in Wichita, KS, and the surrounding areas like Andover and Topeka are sitting on a powerful financial tool that can help alleviate this burden: their home equity.

With property values in Sedgwick County and throughout Kansas seeing steady appreciation over the last few years, you may have more equity than you realize. At The Mortgage Squad, powered by LeaderOne Financial, we specialize in helping clients leverage that equity through a refinance for debt management. Whether you are looking to lower your monthly outflow or simplify your finances, Randy Pitts and his team are here to guide you through the process.

What is Debt Consolidation Refinancing?

Refinancing for debt management, often referred to as a cash-out refinance, involves replacing your current mortgage with a new loan for a higher amount than what you currently owe. The difference between the new loan amount and your existing mortgage balance is given to you in cash. You can then use these funds to pay off high-interest debts such as:

- Credit card balances (often with rates exceeding 20%)

- Personal loans

- Car loans

- Student loans

- Medical bills

By rolling these debts into your mortgage, you are essentially moving high-interest, short-term debt into a lower-interest, long-term secured loan. This can significantly reduce your total monthly payments and improve your cash flow.

The “Wichita Advantage”: Why Now is the Time

The housing market in Kansas has remained resilient. Homeowners in Wichita, Topeka, Andover, and Maize have seen their property values rise, creating a “cushion” of equity.

If you purchased your home a few years ago, your loan-to-value (LTV) ratio might be much lower today due to market appreciation. Accessing this equity via a refinancing solution allows you to reset your financial clock. Instead of making minimum payments on credit cards that barely touch the principal, a debt consolidation refinance allows you to pay off those balances immediately.

The Math: Mortgage Rates vs. Credit Card Rates

Even if current mortgage rates are higher than the historic lows of 2020 or 2021, they are almost always significantly lower than the interest rates on unsecured debt.

Consider this: The average credit card interest rate can hover around 22% to 29%. In contrast, a mortgage rate—even in a fluctuating market—is a fraction of that cost. Furthermore, mortgage interest is often tax-deductible (consult your tax advisor), whereas credit card interest is not.

Comparing Your Options: Cash-Out Refi vs. Other Methods

When looking at debt management strategies, it is important to compare a cash-out refinance against other common tools like Home Equity Lines of Credit (HELOCs) or personal consolidation loans. Here is a breakdown of how they compare:

| Feature | Cash-Out Refinance | HELOC (Home Equity Line of Credit) | Personal Loan | Credit Cards |

|---|---|---|---|---|

| Interest Rate | Typically Lower (Fixed) | Variable (Often higher than 1st mortgage) | Moderate to High (8-15%+) | Very High (20%+) |

| Monthly Payment Stability | Stable (Fixed Rate) | Unstable (Fluctuates with Prime Rate) | Stable (Fixed) | Unstable (Minimums vary) |

| Tax Deductibility | Potential (Interest on home debt) | Potential (If used for home improvements) | None | None |

| Loan Term | 15, 20, or 30 Years | 10 Year Draw / 20 Year Repay | 3 to 7 Years | Indefinite (Revolving) |

| Impact on Cash Flow | High (Lowest monthly payment) | Moderate | Low (Short term = higher payment) | Negative (High interest costs) |

Loan Programs for Debt Consolidation in Kansas

At The Mortgage Squad, we don’t believe in a one-size-fits-all approach. Randy Pitts and David Chittwood offer access to various loan programs that can be used for debt consolidation:

1. Conventional Cash-Out Refinance

This is the most common option for borrowers with good credit (typically 620+). You can usually tap into up to 80% of your home’s value. This is a great option for homeowners in established Wichita neighborhoods looking to consolidate debt and perhaps fund home renovations simultaneously.

2. FHA Cash-Out Refinance

Supported by the Federal Housing Administration, FHA loans are excellent for borrowers who might have lower credit scores. FHA allows you to cash out up to 80% of your home’s value. This can be a lifeline for families needing to restructure their finances to get back on track.

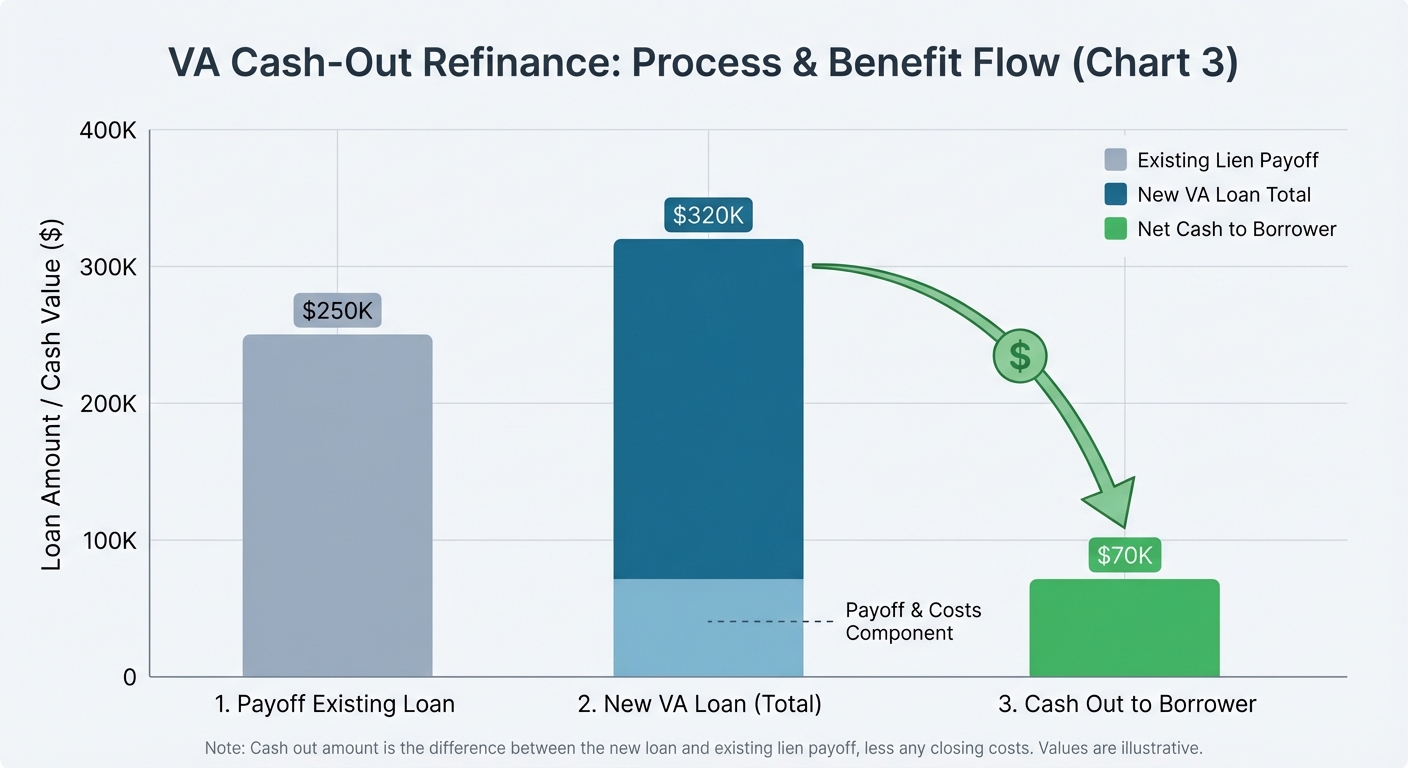

3. VA Cash-Out Refinance

Kansas has a proud military community, from McConnell AFB in Wichita to those serving near Topeka. If you are an eligible veteran or active-duty service member, the VA Cash-Out Refinance is arguably the best product available. It allows qualified borrowers to refinance up to 100% of their home’s value in some cases, often with lower interest rates and no mortgage insurance.

4. Non-QM Loans for Self-Employed

Are you a gig worker, freelancer, or business owner in Wichita? We offer Non-QM loans (Non-Qualified Mortgage) that allow you to qualify using bank statements rather than traditional tax returns. This flexibility ensures that entrepreneurs can also access their equity for debt management.

A Real-World Scenario: The Power of Refinancing

- Current Mortgage: $1,800/month

- Credit Card Debt: $30,000 (at 22% interest) = $900/month minimum payments

- Car Loan: $15,000 (at 8% interest) = $450/month payment

- Total Monthly Outflow: $3,150

The Millers decide to refinance. They take out a new mortgage that pays off their existing home loan plus the $45,000 in consumer debt.

- New Mortgage Payment: $2,300/month (Estimated, including taxes/insurance)

- Old Debt Payments: $0

- New Total Monthly Outflow: $2,300

Total Monthly Savings: $850.

By restructuring their debt, the Millers saved $850 every month. That is over $10,000 a year they can now put toward savings, retirement, or college funds.

The Mortgage Squad Process: Simple, Local, Trusted

Refinancing doesn’t have to be complicated. When you work with Randy Pitts in Wichita or David Chittwood in Topeka, you get a personalized roadmap.

- Consultation: We review your current debts, income, and home equity.

- Appraisal: We order a local appraisal to determine the current market value of your home.

- Underwriting: Our team processes your loan efficiently, keeping you updated via text or email.

- Closing: We schedule a closing at a convenient time. The funds from the new loan are used to pay off your old mortgage and your targeted debts.

Ready to see if you qualify? Check out our Mortgage Calculator to run some preliminary numbers, or reach out directly to start the conversation.

Frequently Asked Questions (FAQs)

1. Will refinancing for debt consolidation hurt my credit score?

Initially, you may see a small dip in your credit score due to the credit inquiry (hard pull) and the new loan opening. However, paying off high-interest revolving debt (like credit cards) significantly lowers your credit utilization ratio, which is a major factor in credit scoring. For many clients, this leads to a rapid and significant increase in their credit score shortly after closing.

2. How much equity do I need to qualify for a cash-out refinance?

Generally, most lenders require you to retain at least 20% equity in your home after the refinance (meaning a maximum Loan-to-Value ratio of 80%). However, VA loans may allow for higher LTV ratios for eligible veterans. Randy Pitts can help you calculate your specific equity position based on recent Wichita market data.

3. Can I use the funds for things other than debt?

Absolutely. While debt management is a smart financial move, the cash you receive is yours. Many homeowners use a portion of the funds to pay off debt and the remainder for home improvements, investing in a second property, or establishing an emergency fund. Visit our Loan Center to explore how investors use these funds.

4. Are there closing costs associated with a refinance?

Yes, just like your original mortgage, there are closing costs (appraisal fees, title insurance, origination fees). However, in a debt consolidation refinance, these costs can typically be rolled into the new loan amount, meaning you rarely have to bring cash to the closing table.

5. Is a refinance better than a debt consolidation loan?

Personal debt consolidation loans often have higher interest rates than mortgages and shorter repayment terms, which can result in high monthly payments. A mortgage refinance offers the lowest possible interest rate and spreads the payments out over a longer term, maximizing your monthly cash flow flexibility.

Take Control of Your Financial Future Today

Don’t let high-interest debt dictate your lifestyle. Your home in Wichita or Topeka is more than just a place to live—it is a financial asset that can work for you. With The Mortgage Squad, you have a partner dedicated to finding the best refinancing solution for your unique situation.

Randy Pitts and the team are ready to help you lower your payments and breathe easier. We are local, we are transparent, and we fight for the best rates for our squad.

Ready to slash your monthly payments?

Get Your Free Refinance Analysis

Or call/text Randy directly at (316) 448-6947.