The 2026 Topeka Renewal Wave: Smart Refinancing Strategies to Avoid Payment Shock

Understanding the Approaching Mortgage Shift for Local Homeowners

For many homeowners in Topeka, Kansas, the upcoming years represent a critical turning point in their financial journey. If you secured a five-year or seven-year Adjustable-Rate Mortgage (ARM) during the record-low rate environment of 2019 through 2021, you might be facing what industry experts call the 2026 renewal wave. As these introductory periods mature, local families are exposed to potential payment shock when their interest rates adjust to current market levels.

At LeaderOne Financial, The Mortgage Squad, we understand that a sudden increase in your monthly housing expense can disrupt your family budget. Being proactive is the best way to protect your financial stability. Here are the key factors driving this shift:

- Expiring ARMs: Low introductory rates transitioning to higher, variable indexes.

- Maturing Temporary Buydowns: Short-term rate reductions that are returning to their permanent note rate.

- Changing Market Conditions: Fluctuations in the broader economic landscape affecting local Topeka real estate.

By partnering with a trusted mortgage lender in Topeka, you can explore personalized refinancing solutions designed to stabilize your payments and keep your dream home affordable.

Breakeven Math and Blended-Rate Guidance for Topeka Families

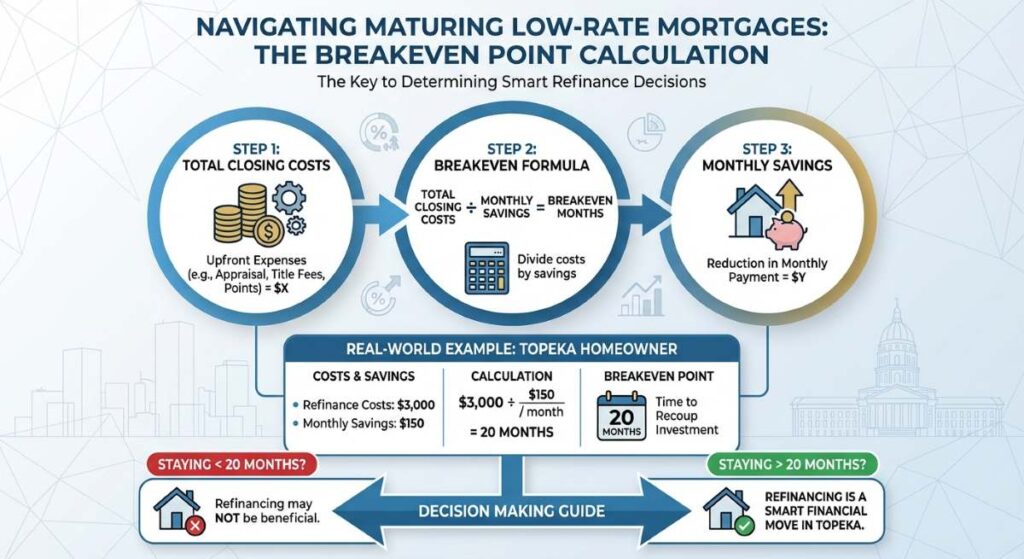

When navigating maturing low-rate mortgages, the most important calculation you can make is your breakeven point. This simple formula divides your total closing costs by your monthly savings to determine how many months it will take to recoup your investment. For example, if a refinance costs $3,000 but saves you $150 per month, your breakeven point is 20 months. If you plan to stay in your Topeka home longer than that timeframe, refinancing is a smart financial move.

However, a traditional refinance is not your only option. If you currently hold a historically low rate on your primary mortgage but need to tap into your home equity or restructure debt to avoid payment shock, a blended-rate strategy might be ideal. Instead of replacing your entire first mortgage, you keep that favorable rate intact and utilize a second mortgage or Home Equity Line of Credit (HELOC). Your blended rate is the weighted average of both loans, often resulting in a significantly lower overall interest expense.

David Chittwood and the team at The Mortgage Squad specialize in these complex calculations, ensuring you have the exact math needed to make an informed decision.

| Strategy | Primary Loan Rate | Secondary Loan Rate | Effective Blended Rate | Best Used For |

|---|---|---|---|---|

| Traditional Refinance | 6.50% (New Rate) | N/A | 6.50% | Securing a fixed rate before an ARM adjusts |

| Blended Rate (HELOC) | 3.25% (Retained) | 8.50% | 4.56% (Estimated) | Accessing equity without losing a low first mortgage rate |

| Temporary Buydown | 4.50% (Year 1) | N/A | Graduated | Easing into a higher rate environment over time |

Timing Your Refinance: Expert Advice from Your Topeka Mortgage Lender

Timing is everything when it comes to mitigating payment shock. Waiting until the exact month your current mortgage adjusts can leave you vulnerable to unpredictable market spikes. As a premier mortgage lender in Topeka, Kansas, David Chittwood recommends reviewing your loan terms at least six to nine months before any scheduled adjustments.

Whether you are exploring conventional loans, FHA options, or specialized Non-QM loans, early preparation allows you to lock in the most advantageous terms. We take pride in offering transparent advice, helping you weigh the pros and cons of acting now versus waiting for potential rate drops.

Your home is one of your greatest assets. Do not let the 2026 renewal wave catch you off guard. Reach out to our Topeka office today to start mapping out your personalized refinancing strategy. LeaderOne Financial, The Mortgage Squad Powered by NMLS ID 12007.

Q1: What is the 2026 mortgage renewal wave?

The 2026 renewal wave refers to the period when many homeowners who secured Adjustable-Rate Mortgages (ARMs) or temporary buydowns between 2019 and 2021 will see their introductory low rates mature and adjust to current, potentially higher market rates.

Q2: How do I calculate my refinancing breakeven point?

You calculate your breakeven point by dividing your total estimated closing costs by your monthly savings from the new loan. This tells you exactly how many months it will take to recover the upfront costs of refinancing.

Q3: What is a blended rate in mortgage refinancing?

A blended rate is the effective interest rate you pay when you keep your existing low-rate first mortgage and take out a second mortgage or HELOC. It is a weighted average of the two rates, allowing you to access equity without losing your original low rate.

Q4: Can I avoid payment shock if my ARM adjusts?

Yes, you can avoid payment shock by proactively refinancing into a fixed-rate mortgage before your ARM adjusts, or by working with a mortgage lender to explore rate buydowns and loan modification strategies.

Q5: Why choose The Mortgage Squad for refinancing in Topeka?

With local expertise from David Chittwood in Topeka, Kansas, The Mortgage Squad offers personalized loan options, transparent breakeven math, and a commitment to finding the best financial solutions for your family.Contact David Chittwood at The Mortgage Squad Today