First-Time Homebuyers in Topeka 2026: Creative Paths to Ownership Using FHA, VA, USDA, and Local Programs

First-Time Homebuyers in Topeka 2026: Creative Paths to Ownership Using FHA, VA, USDA, and Local Programs

Navigating the 2026 Shawnee County Real Estate Market

Stepping into the housing market as a first-time buyer can feel overwhelming, but the 2026 landscape in Topeka, Kansas, is full of opportunity. With the right strategy, securing your dream home in Shawnee County is more achievable than ever. At The Mortgage Squad, our Topeka-based expert, David Chittwood, specializes in helping buyers navigate lower credit thresholds and competitive markets.

Understanding your loan options is the first crucial step:

- FHA Loans: Perfect for buyers with lower credit scores, offering down payments as low as 3.5%.

- VA Loans: A zero-down payment option exclusively for our honored veterans and active military members.

- USDA Loans: Designed for suburban and rural areas, offering 100% financing for eligible properties in and around Shawnee County.

By leveraging these government-backed loans alongside local Kansas down payment assistance programs, you can significantly reduce your upfront costs and compete successfully against other buyers.

Tactical Guidance on Down Payment Assistance and Credit Thresholds

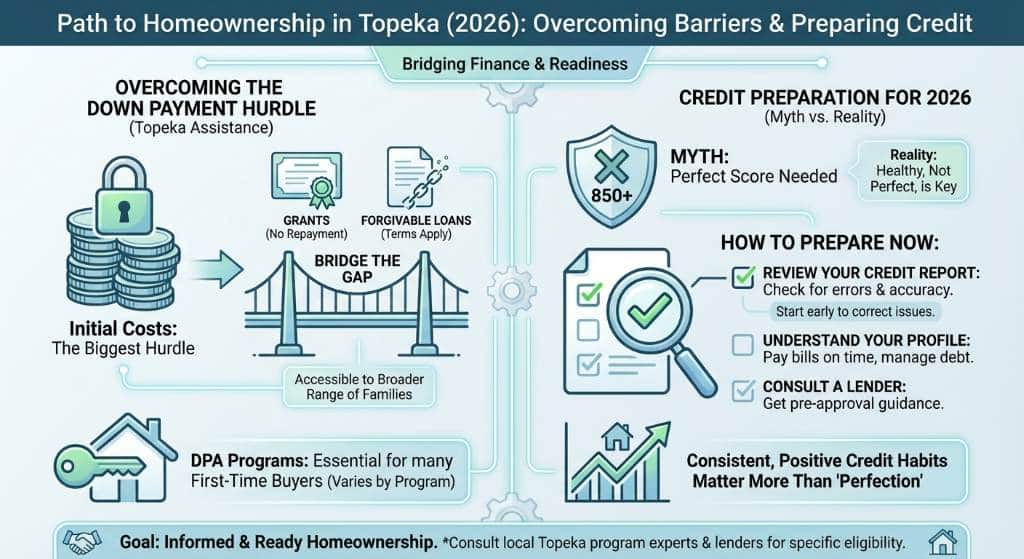

One of the biggest hurdles for first-time homebuyers is saving for the initial costs. Fortunately, there are numerous down payment assistance programs available in Topeka that can bridge the gap. These programs often provide grants or forgivable loans to cover closing costs and down payments, making homeownership accessible to a broader range of families.

When it comes to credit, you do not need a perfect score to buy a home in 2026. Here is how you can prepare:

- Review your credit report: Check for inaccuracies and dispute them immediately.

- Keep utilization low: Aim to keep your credit card balances below 30% of your limit.

- Avoid new debt: Do not open new credit lines while you are in the pre-approval process.

Our team at LeaderOne Financial is dedicated to finding creative paths to ownership, ensuring that lower credit thresholds do not stand in the way of your Topeka home.

| Loan Type | Minimum Down Payment | Typical Minimum Credit Score | Best For |

|---|---|---|---|

| FHA Loan | 3.5% | 580 | Buyers with lower credit scores and limited savings |

| VA Loan | 0% | No strict minimum | Veterans and active-duty military |

| USDA Loan | 0% | 640 | Buyers looking at rural or eligible suburban properties |

| Conventional | 3% to 5% | 620 | Buyers with good credit and moderate savings |

How to Compete Successfully in Shawnee County

The Shawnee County real estate market requires buyers to be strategic and prepared. To stand out among other first-time homebuyers in Topeka, getting pre-approved is non-negotiable. A solid pre-approval letter from a trusted local lender like David Chittwood at The Mortgage Squad signals to sellers that your financing is secure and you are ready to close.

Here are a few tactical tips to win your bid:

- Act quickly: Desirable homes in Topeka move fast. Stay in close contact with your real estate agent and lender.

- Be flexible: If possible, offer flexible closing dates to accommodate the seller’s schedule.

- Rely on local expertise: Working with a local mortgage broker means you have someone who understands the specific nuances of the Kansas market.

By partnering with LeaderOne Financial, you gain access to personalized service, fast closing times, and the competitive edge needed to secure your ideal home.

Q1: What is the minimum credit score for an FHA loan in Topeka?

Generally, you need a minimum credit score of 580 to qualify for an FHA loan with a 3.5% down payment.

Q2: Can I buy a home in Shawnee County with no down payment?

Yes, both VA and USDA loans offer zero-down payment options for eligible buyers in Shawnee County.

Q3: How do down payment assistance programs work in Kansas?

These programs provide grants or secondary loans to help cover your down payment and closing costs, often aimed specifically at first-time homebuyers who meet income and purchase price limits.

Q4: Are USDA loans only for farms?

Not at all. USDA loans are designed for rural and eligible suburban areas, and many residential properties just outside the main Topeka city limits qualify.

Q5: Why should I choose a local mortgage lender in Topeka?

A local lender like David Chittwood at The Mortgage Squad understands the specific Shawnee County market, offers personalized guidance, and can often close loans faster than large national banks.Contact David Chittwood at The Mortgage Squad Today