Is 2026 the Right Year to Buy in Topeka? Beyond the Headlines

Is 2026 the Right Year to Buy in Topeka? Beyond the Headlines

A Contrarian View on Topeka’s Housing Market

When you turn on the evening news, the national housing market can sound intimidating. However, what does that actually mean for buyers right here in Shawnee County? As a trusted mortgage lender in Topeka, LeaderOne Financial and The Mortgage Squad often see a massive disconnect between national headlines and local realities.

While many prospective buyers are waiting on the sidelines for 2026 to bring perfect conditions, taking a contrarian approach could give you a significant advantage. Here is why acting now might be smarter than waiting:

- Less Competition: Fewer buyers actively looking means more negotiating power for you when making an offer.

- Stable Property Values: Topeka continues to show steady, sustainable growth, meaning waiting could cost you more in future equity.

- Flexible Financing: With the right mortgage broker, you can find creative solutions to fit your current budget.

David Chittwood and our local team specialize in navigating these exact market conditions to help you secure the home of your dreams without the stress of trying to time the market perfectly.

Neighborhood Trends and Buyer Opportunities

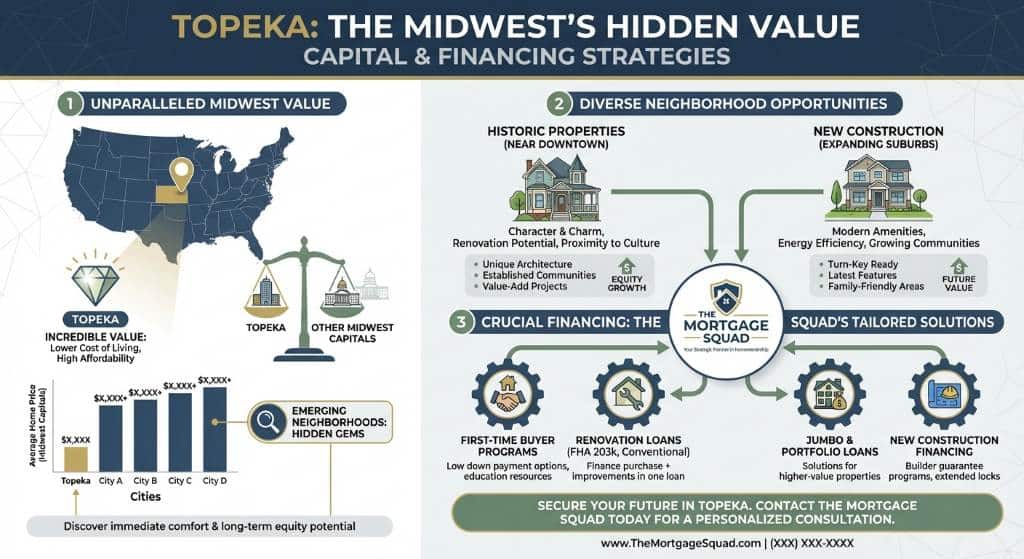

Topeka offers incredible value compared to other capital cities across the Midwest. Buyers who are willing to explore emerging neighborhoods are finding hidden gems that provide both immediate comfort and long-term equity potential.

Whether you are looking at historic properties near downtown or considering new construction in the expanding suburbs, having the right financing strategy is crucial. At The Mortgage Squad, we offer tailored solutions to fit these diverse neighborhood opportunities:

- First-Time Homebuyer Programs: Designed to make your initial purchase smooth, educational, and affordable.

- Down Payment Assistance: Helping to bridge the financial gap for qualified buyers who need extra support.

- Construction Loans: Short-term financing tailored specifically for building a brand new home in a growing subdivision.

By understanding local zoning and development plans, our team can help you position yourself in neighborhoods poised for growth well before the expected 2026 rush begins.

| Loan Program | Minimum Down Payment | Best Suited For | Local Topeka Insight |

|---|---|---|---|

| Conventional | 3% to 5% | Buyers with strong credit scores | Excellent for competitive neighborhoods and standard single-family homes in Topeka. |

| FHA Loans | 3.5% | First-time buyers or those rebuilding credit | Highly popular in emerging Topeka suburbs and for starter homes. |

| VA Loans | 0% | Eligible veterans and active military | Perfect for our strong local military community and veterans in Kansas. |

| USDA Loans | 0% | Rural property buyers | Ideal for properties just outside the main Topeka city limits. |

How to Gain an Edge in the Current Market

Gaining an edge in today’s housing market requires a proactive strategy. Waiting for 2026 might seem like the safe bet, but proactive buyers are utilizing expert guidance to lock in favorable terms right now.

Here are actionable steps to secure your advantage as a homebuyer in Topeka:

- Get Pre-Approved Early: A solid pre-approval from a local expert like David Chittwood shows sellers you are serious and financially ready.

- Explore Non-QM Loans: If you are self-employed or have non-traditional income sources, our Non-QM Loans can offer the flexibility that traditional banks simply cannot provide.

- Partner with Local Experts: A local mortgage banker understands the nuances of Kansas real estate far better than out-of-state call centers.

LeaderOne Financial (NMLS ID 12007) is deeply committed to your success. By working with our Topeka team, you gain access to decades of local knowledge and a highly personalized approach to home financing.

Q1: Will home prices in Topeka drop significantly in 2026?

While national markets fluctuate, Topeka historically maintains steady property values. Waiting for a massive price drop might result in missed opportunities, as local demand remains consistent.

Q2: What are the best loan options for first-time buyers in Topeka?

First-time buyers often benefit from FHA loans, which require a lower down payment, or specific Down Payment Assistance programs we offer at The Mortgage Squad.

Q3: Can I buy a home in Topeka with a low down payment?

Absolutely. Options like VA loans and USDA loans offer zero down payment for qualified buyers, while FHA and certain conventional loans require as little as 3% to 3.5% down.

Q4: How do national interest rates affect the local Kansas market?

National rates influence local mortgage rates, but local housing inventory and demand play a larger role in final home prices. A local mortgage expert can help you navigate rate fluctuations effectively.

Q5: Why should I choose a local mortgage lender over a national bank?

Local lenders like David Chittwood understand the specific nuances of the Topeka market. We offer faster communication, personalized service, and tailored loan products that out-of-state banks simply cannot match.Contact David Chittwood at The Mortgage Squad Today (1-785-450-9056)