Cash-Out Refinancing in 2026: Unlocking Home Equity for Renovations, Investments, or Debt Consolidation

Why 2026 is the Year to Leverage Your Topeka Home Equity

As we navigate the housing market of 2026, homeowners in Topeka and Wichita, Kansas, are sitting on a powerful financial asset: their home equity. With property values maintaining stability and specific market conditions favoring strategic borrowing, a cash-out refinance has become a premier tool for financial optimization. Whether you are looking to update your aging property, consolidate high-interest debt, or expand your real estate portfolio, unlocking your equity can provide the capital you need at a comparatively lower interest rate than other financing options.

At The Mortgage Squad, backed by LeaderOne Financial, we help Kansas homeowners understand how to make their mortgage work for them. David Chittwood, our Topeka-based mortgage banker, emphasizes that 2026 is not just about holding onto a home—it is about utilizing it to build long-term wealth. By replacing your existing mortgage with a new one for a higher amount than you owe, you can pocket the difference in cash to fund major life goals.

Top Strategies for Using Cash-Out Refinance Funds

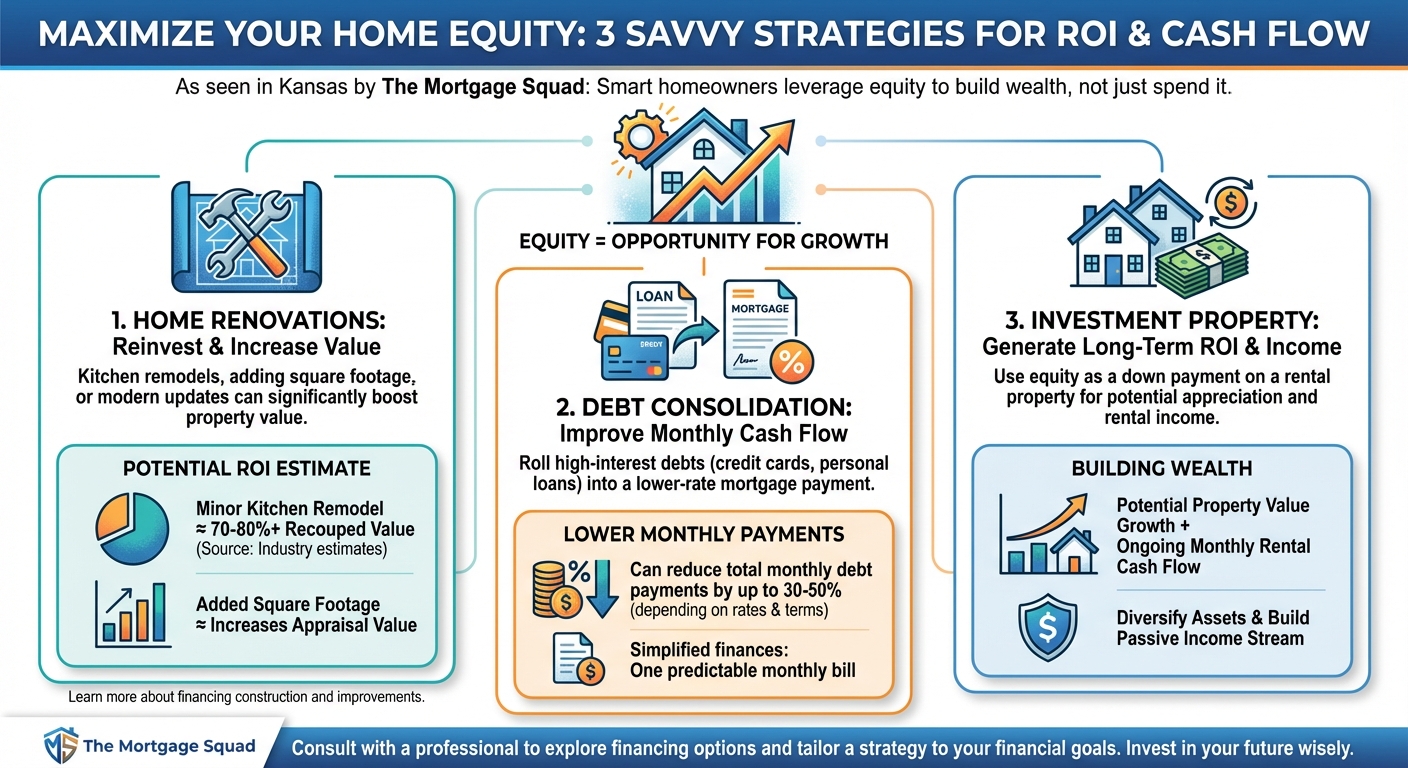

Once you access your equity, how should you use it? The most savvy homeowners in Kansas are using these funds to generate a return on investment (ROI) or improve their monthly cash flow. Here are the three most common strategies we see at The Mortgage Squad:

- Home Renovations: Reinvesting in your property is often the smartest move. Whether it is a kitchen remodel or adding square footage, these projects can increase your home’s value significantly. Learn more about financing construction and improvements in our Construction Loans section.

- Debt Consolidation: With credit card interest rates often hovering near 20% or higher, using mortgage equity (at a much lower rate) to pay off unsecured debt can save you thousands annually. David Chittwood specializes in structuring these loans to lower your total monthly obligations. Check out our Debt Consolidation services.

- Real Estate Investment: 2026 presents unique opportunities for purchasing rental properties. You can use the cash from your primary residence as a down payment on an investment property, effectively growing your portfolio. Explore our Investor Loan programs for more details.

| Financing Option | Average Interest Rate (Est. 2026) | Tax Deductibility | Repayment Term |

|---|---|---|---|

| Cash-Out Refinance | Lower (Mortgage Rates) | Potential (Capital Improvements) | 15-30 Years |

| Credit Cards | 20% – 25%+ | None | Revolving |

| Personal Loans | 10% – 15% | None | 2-5 Years |

| HELOC | Variable (Prime + Margin) | Potential | 10-Year Draw |

Navigating the Process with a Local Topeka Lender

While national lenders offer generic solutions, working with a local expert like David Chittwood in Topeka or Randy Pitts in Wichita ensures you get advice tailored to the Kansas market. Qualifying for a cash-out refinance typically requires you to retain at least 20% equity in your home after the cash is taken out (a maximum 80% Loan-to-Value ratio). Additionally, lenders will look at your debt-to-income (DTI) ratio and credit score to determine your new rate.

It is also important to consider the timing. If current rates are lower than your original mortgage rate, you win twice: you get the cash and potentially lower your interest costs. However, even if rates are slightly higher, the blended savings from paying off high-interest credit cards often makes the math work in your favor. At The Mortgage Squad, we provide a detailed cost-benefit analysis so you can move forward with confidence.

Q1: What is the limit on how much cash I can take out?

typically, you can borrow up to 80% of your home’s appraised value. The cash you receive is the difference between this amount and your remaining mortgage balance.

Q2: Is the cash from a refinance considered taxable income?

No, the IRS generally views these funds as a loan rather than income, so you typically do not have to pay income tax on the cash you receive.

Q3: Can I do a cash-out refinance with a lower credit score?

While conventional loans often require higher scores, FHA and VA cash-out options may be more flexible. Our Non-QM loan options can also assist borrowers with unique credit situations.

Q4: How long does the cash-out refinance process take in Topeka?

The timeline varies, but it typically takes 30 to 45 days from application to closing, depending on the speed of the appraisal and document verification.

Q5: Can I use the funds to buy a second home or investment property?

Absolutely. Many investors use equity from their primary residence to fund down payments for rental properties or vacation homes.Get Your Free Cash-Out Analysis from David Chittwood Today